To help our customers, at HireHop we have done some research into benefits, grants and help you may be entitled to during this very difficult time.

To help our customers, at HireHop we have done some research into benefits, grants and help you may be entitled to during this very difficult time.

In the governments 2020 budget, they announced many schemes to help businesses, some of which will be addressed briefly below and others in more detail at the bottom of the page.

Statutory Sick Pay:

- Small to medium sized businesses and employers can reclaim Statutory Sick Pay (SSP) paid for sickness absence due to COVID-19 for 2 weeks per eligible employee who is off-work.

- For eligible individuals diagnosed with COVID-19 or those who are unable to work because they are self-isolating in line with Government advice, SSP will be payable from day 1 instead of day 4, without any medical proof for 7 days. After 7 days, the businesses need to decide if they need evidence.

Business Rates:

- Business rates retail discount to 100% for one year, expanded to the leisure and hospitality sectors.

- Planned rates discount for pubs of £5,000.

- For guidance, you should contact your local council’s business rates department.

Grants (more detailed at bottom of page):

- Grants of £25,000 to retail, hospitality and leisure businesses operating from smaller premises, with a rateable value over £15,000 and below £51,000.

- A one-off grant of £10,000 to around 700,000 business currently eligible for Small Business Rate Relief or Rural Rate Relief, to help meet ongoing business costs.

Coronavirus Business Interruption Loan Scheme:

- Loan of amount up to £5 million (see bottom of page).

- First 6-month finance interest free (Government to cover interest for first 6 months).

- Government to provide lenders with a guarantee of 80% on each loan (subject to a per-lender cap on claims) without any charge to businesses or banks.

- Provisions to provide further discretionary financial support to businesses.

Support with Tax Affairs:

- All businesses and self-employed people in financial distress, and with outstanding tax liabilities, may be eligible to receive support with their tax affairs through HMRC’s Time To Pay service.

- You can call HMRC’s dedicated helpline on 0800 0159 559 for help and advice.

Mortgage Support:

- Mortgage lenders have agreed they will support customers that are experiencing issues with their finances as a result of Covid-19, including through payment holidays of up to 3 months. Please note that unpaid interest will be added to the mortgage, this is not free money.

Other:

- Relaxation in planning regulations to allow pubs and restaurants to start providing takeaways without a planning application.

- Businesses are encouraged to check their terms of insurance, if they cover for both pandemics and government, as the government and insurance industry confirmed on 17 March 2020, that advice to avoid pubs, theaters etc is sufficient to make a claim.

Cash Grant for Small Businesses

If you are a small business, trading from a rateable business address and qualify for small business rates relief or rural rate relief, you will be entitled to a grant of £10,000. This is basically free money, but only if you are registered for small business rates relief.

Small business rates relief is discount upto 100% on business rates given to businesses who trade from only one premises (a home does not count), or multiple premises where the joint rateable value does not exceed £20,000 (£28,000 for London). You can find your rateable value here. If you have separate limited companies at each depot, each one might qualify, however this is not clear yet.

The rateable value of a property is supposed to be the same as your annual rent. You can easily get Small Business Rates Relief by just phoning your local council who will send you a form that you sign and return. You could even get backdated refunds on past payments if you qualify. Small business rates relief is not automatic, you must apply!

If you don’t qualify for small business rates relief, you may still qualify for the small business multiplier if your rateable value is below £51,000. Again, this is automatic and you need to notify your council, and again you might be entitled to a backdated refund if you qualify.

If your rateable value is around or above £51,000, you should see that per square meter, you are being charged less than far smaller properties in your area, this is due to discount you would naturally get from a landlord for renting so much space. If you feel there is a problem, appeal it yourself here. Don’t use an agent, as the majority will fleece you and demand money indefinitely. All these companies do is fill in online forms and let the VOA (a government department) do the valuation, then charge you fortunes for this.

For companies paying rates, the government is offering a business rates holiday to companies in the hospitality and leisure industry, which by the sound of things, probably does not apply to rental companies who work in that sector. Information is scarce, but it seems for now that this is based on a business premises licensed use, of which a warehouse probably won’t qualify. We still advise calling the business rates team at your local council, as things are changing on a daily basis.

Please note, this only applies to business rates from April 2020 to April 2021 and not previous business rates, so if you are in arrears, you must still pay the arrears, but you might be granted further leniency on your payback schedule if you ask.

Low Interest Loan

From 23rd March 2020, the government has promised loans for SMEs upto £5 million through the British Business Bank, as well as similar loans being offered by many other banks, all 80% underwritten by the government. These are loans and must be paid back. They are also offering to underwrite loans for larger companies, but not much information has been released.

Putting The Company On Hold

This is not ideal, but numerous companies are doing this as they literally have no work. Companies are closing the doors until the storm blows over and paying the employees a reduced rate to stay at home. We are all in this together, and if they want a job after this, they need to help as well. You must get them to sign an agreement that they agree to the reduced pay, otherwise you could find yourself at an employment tribunal.

We are not just suppliers of equipment rental software, we feel that HireHop and our users are all part of a team. We are lucky to have experts in business rates as well as accountancy, and during this difficult time we are more than happy to help our users.

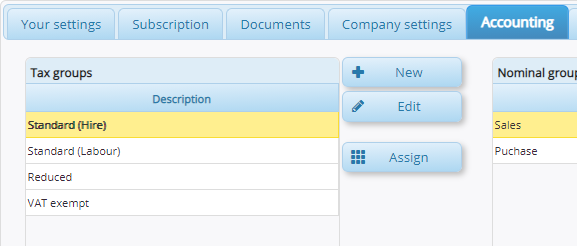

The new HMRC Construction Industry Scheme (CIS) that came into effect on 1st March 2021, means that VAT has to be accounted for differently for CIS registered customers depending on the circumstances. So for one customer for one hire you won’t charge them VAT, yet on another to the same customer, you will charge them VAT. This gets even more confusing when supplying staff with a hire, as the staff element may or may not be subject to normal VAT.

The new HMRC Construction Industry Scheme (CIS) that came into effect on 1st March 2021, means that VAT has to be accounted for differently for CIS registered customers depending on the circumstances. So for one customer for one hire you won’t charge them VAT, yet on another to the same customer, you will charge them VAT. This gets even more confusing when supplying staff with a hire, as the staff element may or may not be subject to normal VAT.